Repo is a generic name for both repurchase transactions and buy/sell-backs.

In a repo, one party sells an asset (usually fixed-income securities) to another party at one price and commits to repurchase the same or another part of the same asset from the second party at a different price at a future date or (in the case of an open repo) on demand. If the seller defaults during the life of the repo, the buyer (as the new owner) can sell the asset to a third party to offset his loss. The asset therefore acts as collateral and mitigates the credit risk that the buyer has on the seller.

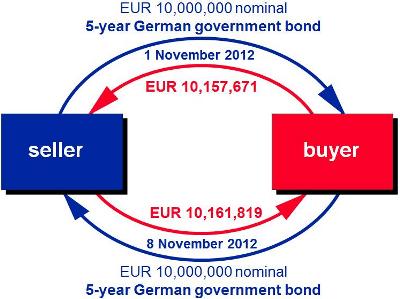

The seller in a repo sells the asset then buys it back, The buyer in a repo buys the asset then sells it back. The buyer is often described as doing a reverse repo.

The buyer receives a collateral to hedge his credit risk on the seller. As the collateral is sold to the buyer, he can liquidate it anytime in case of defaults of the seller without interference from a insolvency court. The buyer can diversify his credit exposure by taking collateral issued by a third party whose credit risk is uncorrelated with the credit risk of the seller. Collateralisation through transfer of title reduces the liquidity risk: if the lender needs liquidity he can sells the (liquid) collateral.

A repo contract also permits to easily find an asset on the market by borrowing it instead of buying it.

The repo is quoted as a negative spread to the reference rate. More precisely, the repo quoted value is the spread of the risk free rate over the repo rate (and not the spread of the repo rate over the risk free rate).

A repo quotation of 20bps means that the repo rate is 20bps lower than the reference rate.

The repo rate is then obtained as the reference (risk free) rate minus the quoted repo spread.

Repo rate may be negative meaning that investor are keen to pay to borrow collaterals or more specifically to obtain the collateral without having it on its balance sheet.

Repo offers deposits secured by legal title to high-quality liquidity assets (HQLAs) and includes lenders other than commercial banks. It allows deeper and cheaper funding, easier and more reliable short-term funding (lowering costs). It also allows institutional investors to meet temporary liquidity requirements without having to liquidate strategic long-term investment.

Repo is a more stable source of short-term wholesale funding than unsecured deposits. It lowers both credit and liquidity risk. This means lenders are more willing to offer longer-term funding and are less likely to refuse to roll-over lending, even in a stressed market. The stability of repo funding is reinforced by the wide range of lenders who are willing to lend in the wholesale money market. Repo also mitigates systemic risk by allowing traders and investors who need liquidity in a stressed market to convert assets temporarily into cash in a way that is less disruptive than outright sales. Outright sales would depress the price of collateral securities and crystallize any unrealised losses on the holdings being liquidated or on hedges that have to be unwound when holdings are sold.

The capacity of repo collateralised by HQLA to mitigate credit and liquidity risks is particularly valued by risk-averse money market investors seeking a secure and liquid investment (investors such as Money Market Mutual Fund, Asset Managers, large Non-Financial Corporates, …). Repo is also the most secure short-term asset available to many such investors that do not have access to risk-free deposit accounts at central banks. While treasury bills could provide an alternative risk-free investment to repo, in most countries, the supply of treasury bills is oversubscribed by investors who hold these bills to maturity. This makes the secondary market narrow and forces investors to compete in the crowded primary market, which (like most money market securities) offers only a few tenors, whereas repo offers a full range of maturity dates without broken date penalties or premiums.

The nature of the repo market allows the use, for the central bank, of a wider range of assets than outright purchase. The collateralised nature of the repo market reduces the credit risk of the central bank. Central bank repo can feed seamlessly into the interdealer repo market through which liquidity can be efficiently redistributed to banks and non-banks. Central banks buy repo to add liquidity in the market and sell repo to remove liquidity from the market. In periods of market stress, Central banks act as lender of last resort through the repo market.

Institutional investors such as alternative investment funds (hedge funds) borrow cash in the repo market to fund leveraged investment strategies on a cost-efficient basis and also borrow securities to allow them to take short positions. These funds play an important role in feeding market liquidity and driving price discovery through trading and arbitrage, and their ability to borrow securities to sell short is important in helping to stop asset price bubbles from developing.

In the primary debt market, repo allows dealers to fund their bids at bond auctions and their underwriting positions in syndicated bond issues at reasonable cost, thereby providing cheaper and less risky access to the capital markets for issuers, both governments and corporates.

Investors in corporate bonds often seek to neutralize their exposure to general interest rate movements in order to target just the credit risk of these securities in the form of the credit spread. This can be done by taking a short position in the benchmark government bond with the closest duration to the corporate bond. This short position is done by borrowing in the repo market.

Market makers insure liquidity in the secondary market by quoting immediately executable prices at which they are committed to trade on demand. Repo market helps market maker in two manner:

The repo market fosters price discovery by facilitating primary market activity but, most crucially, by feeding liquidity in the secondary market, which fosters trading and arbitrage. At a technical level, repo rates are a key component of the cost of carry of long and short positions in securities, and thus of the forward prices that measure the relative value of a security. Repo itself can be used to arbitrage inconsistent valuations between securities from the same issuer of similar maturity and thereby generate an accurate yield curve. In addition, repo links the money and capital markets, creating a continuous yield curve. Accurate and complete yield curves are essential for the correct pricing of other financial instruments and thus the efficient allocation of capital by financial markets.

The use of repo to efficiently fund long positions in securities and cover short positions is fundamental to the hedging and pricing of derivatives, given that securities are the ultimate hedge for their own derivatives.

If an intermediary has sold securities to one party which it has purchased from another, but the inward delivery fails to arrive on time, the intermediary can borrow those securities in the repo market to ensure that it can make timely delivery to the first party until such time as the second party delivers or an alternative purchase can be made from a third party.

Squeezez describe situations in which numerous short sellers purchase stock to cover losses or when numerous investors sell long positions to take capital gains off the table. These situation create or exacerbate temporary imbalances between supply and demand. Squeezes can lead to settlement failures and disorderly markets.

By allowing the borrowing of securities, repo helps to prevent individual institutions ‘squeezing’ the market in a particular security.

Repo allows efficient mobilization and allocation of collateral: if a firm does not include the type of security required as collateral it can exchange the securities it does hold for those that it needs by using a repo to lend what it has and a reverse repo to borrow what it needs. Traditional demand for collateral is being increased by the wider use of SFTs and regulatory requirements to hold larger liquidity reserves and to either centrally-clear or collateralise OTC derivatives.

EUR 3 trillion per day (also seen USD 6 trillion per day)

Repo is traditionally short-term instruments with a bulk of liquidity relatively short-term, reflecting its core role in funding securities dealers. The US repo market is mainly overnight.

GC or general collateral is a set or basket of security issues which trade in the repo market at the same or a very similar repo rate, which is called the GC repo rate. GC securities can therefore be substituted for one another without changing the repo rate much, if at all. In other words, the buyer in a GC repo is indifferent to which of the GC securities he will receive.

The fact that GC securities can be substituted for one another means that the driver of the GC repo rate is not the supply and demand of particular issues of securities, but of cash. For this reason, GC repo is sometimes called cash-driven repo. As a measure of the cost of borrowing cash, the GC repo rate is highly correlated with unsecured money market interest rates.

The basket of security issues that form a particular GC repo market belong to the same class. For example, in the US, there is Treasury GC, Agency Debt GC and Agency MBS GC.

A special is an issue of securities that is subject to exceptional demand in the repo and cash markets compared with very similar issues. Competition to buy or borrow a special causes potential buyers in the repo market to offer cheap cash in exchange. A special is therefore identified by a repo rate that is distinctly lower than the general collateral repo rate. The demand for some specials can become so strong that the repo rate on that particular issue falls to zero or even goes negative in an otherwise positive interest rate environment. The repo market is the only financial market in which, historically, a negative rate of return has not been unusual. Reasons for an asset to be subject to exceptional demand include:

During the life of a repo, the buyer holds legal title to the collateral. In other words, the collateral is his property. He is therefore entitled to any benefits of ownership, including any coupons, dividends or other income that may be paid by the issuer of the collateral. However, the seller of collateral retains the risk on the collateral, as he has committed to buy it back in the future for its original value plus repo interest (so, if the price falls between selling and buying, the seller will suffer the loss and vice versa). The seller would not accept the risk on the collateral unless he also receives the return, including coupons, dividends or other income. To satisfy the seller, under the ICMA’s Global Master Repurchase Agreement (GMRA), in the case of repurchase transactions, the buyer agrees to immediately pay compensatory amounts to the seller equivalent to any income payment received on the collateral.

The repo rate is mainly impacted by either cash demand for General collateral or the liquidity (supply and demand) of the collateral for special.

Different derivatives of asset use repo in their pricing:

See: